Understanding California’s Property Taxes(转)

Jennifer-1157 11/12 270152

November 29, 2012

Understanding California’s Property Taxes

Executive Summary

The various taxes and charges on a California property tax bill are complex and often not well understood. This report provides an overview of this major source of local government revenue and highlights key policy issues related to property taxes and charges.

A Property Tax Bill Includes a Variety of Different Taxes and Charges. A typical California property tax bill consists of many taxes and charges including the 1 percent rate, voter–approved debt rates, parcel taxes, Mello–Roos taxes, and assessments. This report focuses primarily on the 1 percent rate, which is the largest tax on the property tax bill and the only rate that applies uniformly across every locality. The taxes due from the 1 percent rate and voter–approved debt rates are based on a property’s assessed value. The California Constitution sets the process for determining a property’s taxable value. Although there are some exceptions, a property’s assessed value typically is equal to its purchase price adjusted upward each year by 2 percent. Under the Constitution, other taxes and charges may not be based on the property’s value.

The Property Tax Is One of the Largest Taxes Californians Pay. In some years, Californians pay more in property taxes and charges than they do in state personal income taxes, the largest state General Fund revenue source. Local governments collected about $43 billion in 2010–11 from the 1 percent rate. The other taxes and charges on the property tax bill generated an additional $12 billion.

The Property Tax Base Is Diverse. Property taxes and charges are imposed on many types of property. For the 1 percent rate, owner–occupied residential properties represent about 39 percent of the state’s assessed value, followed by investment and vacation residential properties (34 percent) and commercial properties (28 percent). Certain properties—including property owned by governments, hospitals, religious institutions, and charitable organizations—are exempt from the 1 percent property tax rate.

All Revenue From Property Taxes Is Allocated to Local Governments. Property tax revenue remains within the county in which it is collected and is used exclusively by local governments. State laws control the allocation of property tax revenue from the 1 percent rate to more than 4,000 local governments, with K–14 districts and counties receiving the largest amounts. The distribution of property tax revenue, however, varies significantly by locality.

The Property Tax Has a Significant Effect on the State Budget. Although the property tax is a local revenue source, it affects the state budget due to the state’s education finance system—additional property tax revenue from the 1 percent rate for K–14 districts generally decreases the state’s spending obligation for education. Over the years, the state has changed the laws regarding property tax allocation many times in order to reduce its costs for education programs or address other policy interests.

The State’s Current Property Tax Revenue Allocation System Has Many Limitations. The state’s laws regarding the allocation of property tax revenue from the 1 percent rate have evolved over time through legislation and voter initiatives. This complex allocation system is not well understood, transparent, or responsive to modern local needs and preferences. Any changes to the existing system, however, would be very difficult.

California’s Property Tax System Has Strengths and Limitations. Economists evaluate taxes using five common tax policy criteria—growth, stability, simplicity, neutrality, and equity. The state’s property tax system exhibits strengths and limitations when measured against these five criteria. Since 1979, revenue from the 1 percent rate has exceeded growth in the state’s economy. Property tax revenue also tends to be less volatile than other tax revenues in California due to the acquisition value assessment system. (Falling real estate values during the recent recession, however, caused some areas of the state to experience declines in assessed value and more volatility than in the past.) Although California’s property tax system provides governments with a stable and growing revenue source, its laws regarding property assessment can result in different treatment of similar taxpayers. For example, newer property owners often pay a higher effective tax rate than people who have owned their homes or businesses for a long time. In addition, the property tax system may distort business and homeowner decisions regarding relocation or expansion.

Introduction

For many California taxpayers, the property tax bill is one of the largest tax payments they make each year. For thousands of California local governments—K–12 schools, community colleges, cities, counties, and special districts—revenue from property tax bills represents the foundation of their budgets.

Although property taxes and charges play a major role in California finance, many elements of this financing system are complex and not well understood. The purpose of this report is to serve as an introductory reference to this key funding source. The report begins by explaining the most common taxes and charges on the property tax bill and how these levies are calculated. It then describes how the funds collected from property tax bills—$55 billion in 2010–11—are distributed among local governments. Last, because California’s property taxation system has evoked controversy over the years, the report provides a framework for evaluating it. Specifically, we examine California property taxes relative to the criteria commonly used by economists for reviewing tax systems, including revenue growth, stability, simplicity, neutrality, and equity. The report is followed with an appendix providing further detail about the allocation of property tax revenue.

What Is on the Property Tax Bill?

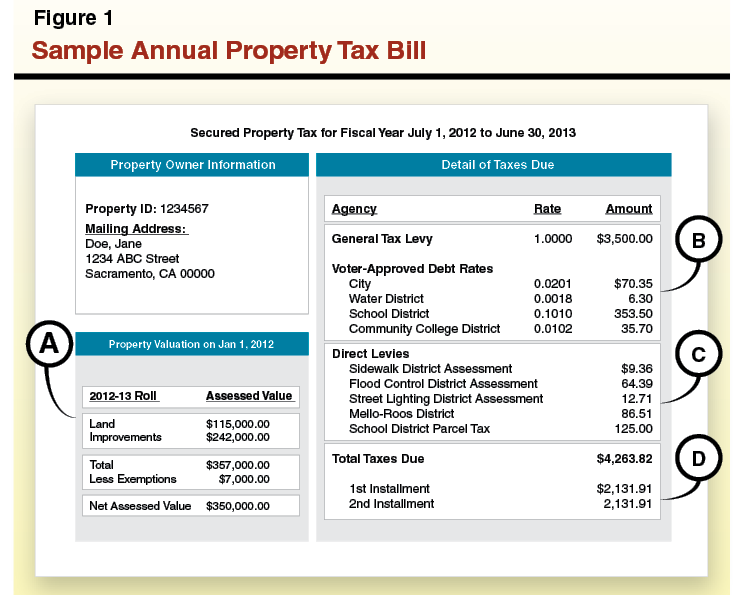

A California property tax bill includes a variety of different taxes and charges. As shown on the sample property tax bill in Figure 1, these levies commonly include:

- The 1 percent rate established by Proposition 13 (1978).

- Additional tax rates to pay for local voter–approved debt.

- Property assessments.

- Mello–Roos taxes.

- Parcel taxes.

The Constitution establishes a process for determining a property’s taxable value for purposes of calculating tax levies from the 1 percent rate and voter–approved debt. In our sample property tax bill, “Box A” identifies the taxable value of the property and “Box B” shows the property’s tax levies that are calculated based on this value. Levies based on value—such as the 1 percent rate and voter–approved debt rates—are known as “ad valorem” taxes.

Under the Constitution, other taxes and charges on the property tax bill (shown in “Box C”) may not be based on the property’s taxable value. Instead, they are based on other factors, such as the benefit the property owner receives from improvements.

As shown in “Box D,” the total amount due on most property tax bills is divided into two equal amounts. The first payment is due by December 10 and the second payment is due by April 10.

How Are Property Taxes and Charges Determined?

Ad valorem property taxes—the 1 percent rate and voter–approved debt rates—account for nearly 90 percent of the revenue collected from property tax bills in California. Given their importance, this section begins with an overview of ad valorem taxes and describes how county assessors determine property values. Later in the chapter, we discuss the taxes and charges that are determined based on factors other than property value.

Taxes Based on Property Value

The 1 Percent Rate. The largest component of most property owners’ annual property tax bill is the 1 percent rate—often called the 1 percent general tax levy or countywide rate. The Constitution limits this rate to 1 percent of assessed value. As shown on our sample property tax bill, the owner of a property assessed at $350,000 owes $3,500 under the 1 percent rate. The 1 percent rate is a general tax, meaning that local governments may use its revenue for any public purpose.

Voter–Approved Debt Rates. Most tax bills also include additional ad valorem property tax rates to pay for voter–approved debt. Revenue from these taxes is used primarily to repay general obligation bonds issued for local infrastructure projects, including the construction and rehabilitation of school facilities. (As described in the nearby box, some voter–approved rates are used to pay obligations approved by local voters before 1978.) Bond proceeds may not be used for general local government operating expenses, such as teacher salaries and administrative costs. Most local governments must obtain the approval of two–thirds of their local voters in order to issue general obligation bonds repaid with debt rates. General obligation bonds for school and community college facilities, however, may be approved by 55 percent of the school or community college district’s voters. Local voters do not approve a fixed tax rate for general obligation bond indebtedness. Instead, the rate adjusts annually so that it raises the amount of money needed to pay the bond costs.

Debt Approved by Voters Prior to 1978

The California Constitution allows local governments to levy voter–approved debt rates—ad valorem rates above the 1 percent rate—for two purposes. The first purpose is to pay for indebtedness approved by voters prior to 1978, as allowed under Proposition 13 (1978). Proposition 42 (1986) authorized a second purpose by allowing local governments to levy additional ad valorem rates to pay the annual cost of general obligation bonds approved by voters for local infrastructure projects. Because most debt approved before 1978 has been paid off, most voter–approved debt rates today are used to repay general obligation bonds issued after 1986 as authorized under Proposition 42.

Some local governments, however, continue to levy voter–approved debt rates for indebtedness approved by voters before 1978. While most bonds issued before the passage of Proposition 13 have been paid off, state courts have determined that other obligations approved by voters before 1978 also can be paid with an additional ad valorem rate. Two common pre–1978 obligations paid with voter–approved debt rates are local government employee retirement costs and payments to the State Water Project.

Voter–Approved Retirement Benefits. Voters in some counties and cities approved ballot measures or city charters prior to 1978 that established retirement benefits for local government employees. The California Supreme Court ruled that such pension obligations represent voter–approved indebtedness that could be paid with an additional ad valorem rate. Local governments may levy the rate to cover pension benefits for any employee, including those hired after 1978, but not to cover any enhancements to pension benefits enacted after 1978. Local governments may adjust the rate annually to cover employee retirement costs, but state law limits the rate to the level charged for such purposes in 1982–83 or 1983–84, whichever is higher. A recent review shows that at least 20 cities and 1 county levy voter–approved debt rates to pay some portion of their annual pension costs. The rates differ by locality. For example, the City of Fresno’s voter–approved debt rate for employee retirement costs is 0.03 percent of assessed value in 2012–13, while the City of San Fernando’s rate is 0.28 percent.

State Water Project Payments. Local water agencies can levy ad valorem rates above the 1 percent rate to pay their annual obligations for water deliveries from the State Water Project. State courts concluded that such costs were voter–approved debt because voters approved the construction, operation, and maintenance of the State Water Project in 1960. As a result, most water agencies that have contracts with the State Water Project levy a voter–approved debt rate.

Property tax bills often include more than one voter–approved debt rate. In our sample property tax bill, for example, the property owner is subject to four additional rates because local voters have approved bond funds for the city and water, school, and community college districts where the property is located. These rates tend to be a small percentage of assessed value. Statewide, the average property tax bill includes voter–approved debt rates that total about one–tenth of 1 percent of assessed value.

Calculating Property Value for Ad Valorem Taxes

One of the first items listed on a property tax bill is the assessed value of the land and improvements. Assessed value is the taxable value of the property, which includes the land and any improvements made to the land, such as buildings, landscaping, or other developments. The assessed value of land and improvements is important because the 1 percent rate and voter–approved debt rates are levied as a percentage of this value, meaning that properties with higher assessed values owe higher property taxes.

Under California’s tax system, the assessed value of most property is based on its purchase price. Below, we describe the process county assessors use to determine the value of local “real property” (land, buildings, and other permanent structures). This is followed by an explanation of how assessors determine the value of “personal property” (property not affixed to land or structures, such as computers, boats, airplanes, and business equipment) and “state assessed property” (certain business properties that cross county boundaries).

Local Real Property Is Assessed at Acquisition Value and Adjusted Upward Each Year. The process that county assessors use to determine the value of real property was established by Proposition 13. Under this system, when real property is purchased, the county assessor assigns it an assessed value that is equal to its purchase price, or “acquisition value.” Each year thereafter, the property’s assessed value increases by 2 percent or the rate of inflation, whichever is lower. This process continues until the property is sold, at which point the county assessor again assigns it an assessed value equal to its most recent purchase price. In other words, a property’s assessed value resets to market value (what a willing buyer would pay for it) when it is sold. (As shown in Figure 2, voters have approved various constitutional amendments that exclude certain property transfers from triggering this reassessment.)

Figure 2

Property Transfers That Do Not Trigger Reassessment

Proposition | Year | Description |

3 | 1982 | Allows property owners whose property has been taken by eminent domain proceedings to transfer their existing assessed value to a new property of similar size and function. |

50 | 1986 | Allows property owners whose property has been damaged or destroyed in a natural disaster to transfer their existing assessed value to a comparable replacement property within the same county. |

58 | 1986 | Excludes property transfers between spouses or between parents and children from triggering reassessment. |

60 | 1986 | Allows homeowners over the age of 55 to transfer their existing assessed value to a new home, of equal or lesser market value, within the same county. |

90 | 1988 | Extends Proposition 60 by allowing homeowners to transfer their existing assessed value to a new home, of equal or lesser market value, in a different participating county. |

110 | 1990 | Allows disabled homeowners to transfer their existing assessed value from an existing home to a newly purchased home of equal or lesser market value. |

171 | 1993 | Extends Proposition 50 by allowing property owners affected by a natural disaster to transfer their existing assessed value to a comparable replacement property in a different participating county. |

193 | 1996 | Excludes property transfers between grandparents and grandchildren (when the parents are deceased) from triggering reassessment. |

1 | 1998 | Allows property owners whose property is made unusable by an environmental problem to transfer their existing assessed value to a comparable replacement property. |

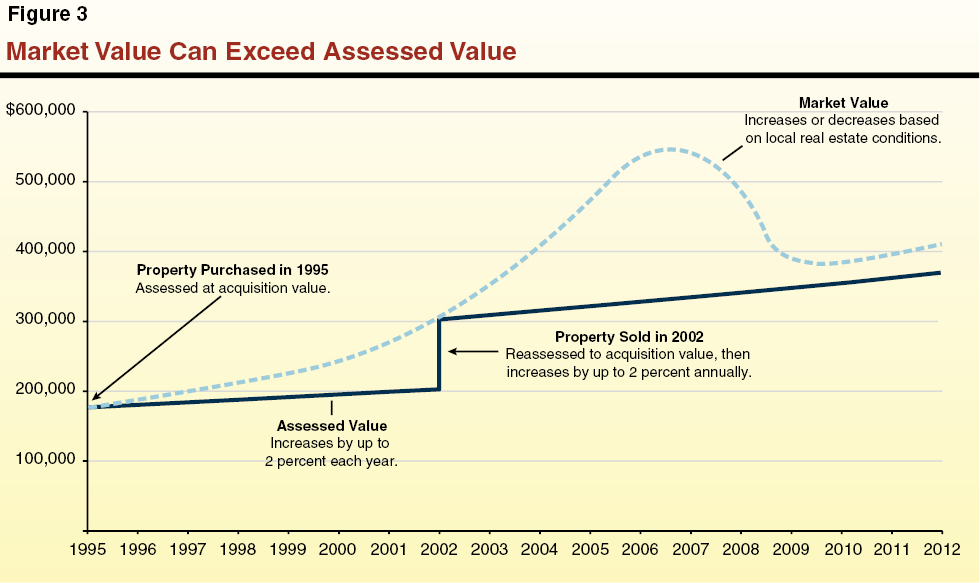

In most years, under this assessment practice, a property’s market value is greater than its assessed value. This occurs because assessed values increase by a maximum of 2 percent per year, whereas market values tend to increase more rapidly. Therefore, as long as a property does not change ownership, its assessed value increases predictably from one year to the next and is unaffected by higher annual increases in market value. For example, Figure 3 shows how a hypothetical property purchased in 1995 for $185,000 would be assessed in 2012. Although the market value of the property increased to $300,000 by 2002, the assessed value was $200,000 because assessed value grew by only up to 2 percent each year. Upon being sold in 2002, the property’s assessed value reset to a market value of $300,000. Because of the large annual increase in home values after 2002, however, the market value was soon much greater than the assessed value for the new owner as well.

Property Improvements Are Assessed Separately. When property owners undertake property improvements, such as additions, remodeling, or building expansions, the additions or upgrades are assessed at market value in that year and increase by up to 2 percent each year thereafter. The unimproved portion of the property continues to be assessed based on its original acquisition value. For example, if a homeowner purchased a home in 2002 and then added a garage in 2010, the home and garage would be assessed separately. The original property would be assessed at its 2002 acquisition value adjusted upward each year while the garage would be assessed at its 2010 market value adjusted upward. The property’s assessed value would be the combined value of the two portions. (As shown in Figure 4, voters have excluded certain property improvements from increasing the assessed value of a property.)

Figure 4

Property Improvements That Do Not Increase a Property’s Assessed Value

Constitutional Amendments Approved After June 1978

Proposition | Year | Type of Improvement |

8 | 1978 | Reconstruction following natural disaster |

7 | 1980 | Solar energy construction |

31 | 1984 | Fire–safety improvements |

110 | 1990 | Accessibility construction for disabled homeowners |

177 | 1994 | Accessibility construction for any property |

1 | 1998 | Reconstruction following environmental contamination |

13 | 2010 | Seismic safety improvements |

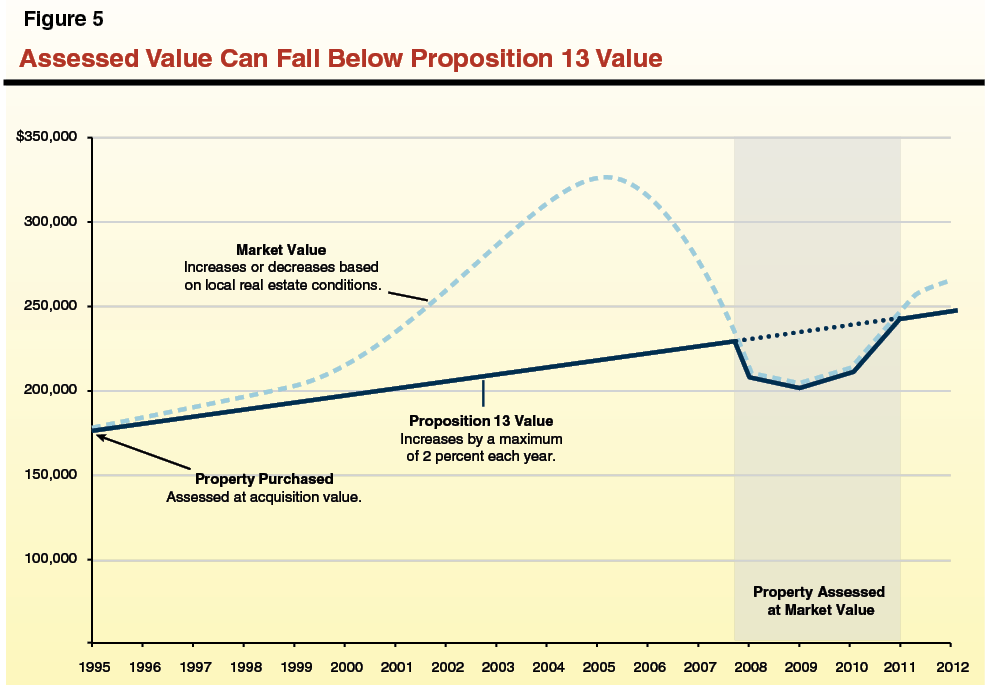

Assessed Value May Be Reduced When Market Values Fall Significantly. When real estate values decline or property damage occurs, a property’s market value may fall below its assessed value as set by Proposition 13. Absent any adjustment to this assessed value, the property would be taxed at a greater value than it is worth.

In these events, county assessors may automatically reduce the Proposition 13 assessed value of a property to its current market value. If they do not, however, a property owner may petition the assessor to have his or her assessed value reduced. These decline–in–value properties are often called “Prop 8 properties” after Proposition 8 (1978), which authorizes this assessment reduction to market value. Figure 5 illustrates the assessment of a hypothetical decline–in–value property over time. The market value of the property purchased in 1995 stays above its Proposition 13 assessed value through 2007. A significant decline, however, drops the property’s market value below its Proposition 13 assessed value. At this time, the property receives a decline–in–value assessment (equal to its market value) that is less than its Proposition 13 assessment. For three years, the property is assessed at market value, which may increase or decrease by any amount. By 2012, the property’s market value once again exceeds what its assessed value would have been absent Proposition 8 (acquisition price plus the 2 percent maximum annual increase). In subsequent years, the property’s assessed value is determined by its acquisition price adjusted upward each year.

Homeowners Are Eligible for a Property Tax Exemption. Homeowners may claim a $7,000 exemption from the assessed value of their primary residence each year. As shown in “Box A” of the sample property tax bill in Figure 1, this exemption lowers the assessed value of the homeowner’s land and improvements by $7,000, reducing taxes under the 1 percent rate by $70 and reducing taxes from voter–approved debt rates by a statewide average of $8.

Two Types of Property Are Assessed at Their Market Value. Two categories of property are assessed at their current market value, rather than their acquisition value: personal property and state– assessed property. (We provide more information about these properties in the nearby box.)Combined, these types of properties accounted for 6 percent of statewide–assessed value in 2011–12. Most personal property and state–assessed property is taxed at the 1 percent rate plus any additional rates for voter–approved debt.

Properties Assessed at Current Market Value

Personal Property. Personal property is property other than land, buildings, and other permanent structures, which are commonly referred to as “real property.” Most personal property is exempt from property taxation, including business inventories, materials used to manufacture products, household furniture and goods, personal items, and intangible property like gym memberships and life insurance policies. Some personal property, however, is subject to the property tax. These properties consist mainly of manufacturing equipment, business computers, planes, commercial boats, and office furniture. When determining the market value of personal property, county assessors take into account the loss in value due to the age and condition of personal property—a concept known as depreciation. Unlike property taxes on real property, which are due in two separate payments, taxes on personal property are due on July 3.

State–Assessed Property. The State Board of Equalization is responsible for assessing certain real properties that cross county boundaries, such as pipelines, railroad tracks and cars, and canals. State–assessed properties are assessed at market value and, with the exception of railroad cars, taxed at the 1 percent rate plus any additional rates for voter–approved debt. (As part of a federal court settlement decades ago, railroad cars are taxed at a rate that is somewhat lower than 1 percent. The railcar tax rate varies each year and currently is about 0.8 percent.)

Determining Other Taxes and Charges

All other taxes and charges on the property tax bill are calculated based on factors other than the property’s assessed value. For example, some levies are based on the cost of a service provided to the property. Others are based on the size of a parcel, its square footage, number of rooms, or other characteristics. Below, we discuss three of the most common categories of non–ad valorem levies: assessments, parcel taxes, and Mello–Roos taxes. In addition to these three categories, some local governments collect certain fees for service on property tax bills, such as charges to clear weeds on properties where the weeds present a fire safety hazard. These fees are diverse and relatively minor, and therefore are not examined in this report.

Assessments. Local governments levy assessments in order to fund improvements that benefit real property. For example, with the approval of affected property owners, a city or county may create a street lighting assessment district to fund the construction, operation, and maintenance of street lighting in an area. Under Proposition 218 (1996), improvements funded with assessments must provide a direct benefit to the property owner. An assessment typically cannot be levied for facilities or services that provide general public benefits, such as schools, libraries, and public safety, even though these programs may increase the value of property. Moreover, the amount each property owner pays must reflect the cost incurred by the local government to provide the improvement and the benefit the property receives from it. To impose a new assessment, a local government must secure the approval of a weighted majority of affected property owners, with each property owner’s vote weighted in proportion to the amount of the assessment he or she would pay.

Parcel Taxes. With the approval of two–thirds of voters, local governments may impose a tax on all parcels in their jurisdiction (or a subset of parcels in their jurisdiction). Local governments typically set parcel taxes at fixed amounts per parcel (or fixed amounts per room or per square foot of the parcel). Unlike assessments, parcel tax revenue may be used to fund a variety of local government services, even if the service does not benefit the property directly. For example, school districts may use parcel tax revenue to pay teacher salaries or administrative costs. The use of parcel tax revenue, however, is restricted to the public programs, services, or projects that voters approved when enacting the parcel tax.

Mello–Roos Taxes. Mello–Roos taxes are a flexible revenue source for local governments because they (1) may be used to fund infrastructure projects or certain services; (2) may be levied in proportion to the benefit a property receives, equally on all parcels, by square footage, or by other factors; and (3) are collected within a geographical area drawn by local officials.

Local governments often use Mello–Roos taxes to pay for the public services and facilities associated with residential and commercial development. This occurs because landowners may approve Mello–Roos taxes by a special two–thirds vote—each owner receiving one vote per acre owned—when fewer than 12 registered voters reside in the proposed district. In this way, a developer who owns a large tract of land could vote to designate it as a Mello–Roos district. After the land is developed and sold to residential and commercial property owners, the new owners pay the Mello–Roos tax that funds schools, libraries, police and fire stations, or other public facilities and services in the new community. Mello–Roos taxes are subject to two–thirds voter approval when there are 12 or more voters in the proposed district.

What Properties Are Taxed?

Property taxes and charges are imposed on many types of properties. These properties include common types such as owner–occupied homes and commercial office space, as well as less common types like timeshares and boating docks. In the section below, we describe the state’s property tax base—the types of real properties that are subject to the 1 percent rate and the share of total assessed value that each property type represents.

Due to data limitations, we do not summarize the tax bases of other taxes and charges. We note, however, that the property tax base for other taxes and charges is different from the tax base for the 1 percent rate. This is because the 1 percent rate applies uniformly to all taxable real property, whereas other taxes and charges are levied at various levels and on various types of property throughout the state (according to local voter or local government preferences). For example, if a suburban school district levies a parcel tax on each parcel in a residential area, the owners of single–family homes would pay a large share of the total parcel taxes. Accordingly, the school district’s parcel tax base would be more heavily residential than the statewide property tax base under the 1 percent rate (which applies to all taxable property).

What Properties Are Subject to the 1 Percent Rate?

Although most real property is taxable, the Constitution exempts certain types of real property from taxation. In general, these are government properties or properties that are used for non–commercial purposes, including hospitals, religious properties, charities, and nonprofit schools and colleges. California properties that are subject to the property tax, however, can be classified in three ways:

- Owner–occupied residential—properties that receive the state’s homeowner’s exemption, which homeowners may claim on their primary residence.

- Investment and vacation residential—residential properties other than those used as a primary residence, including multifamily apartments, rental condominiums, rental homes, vacant residential land, and vacation homes.

- Commercial—retail properties, industrial plants, farms, and other income–producing properties.

Distribution of the Tax Base for the 1 Percent Rate

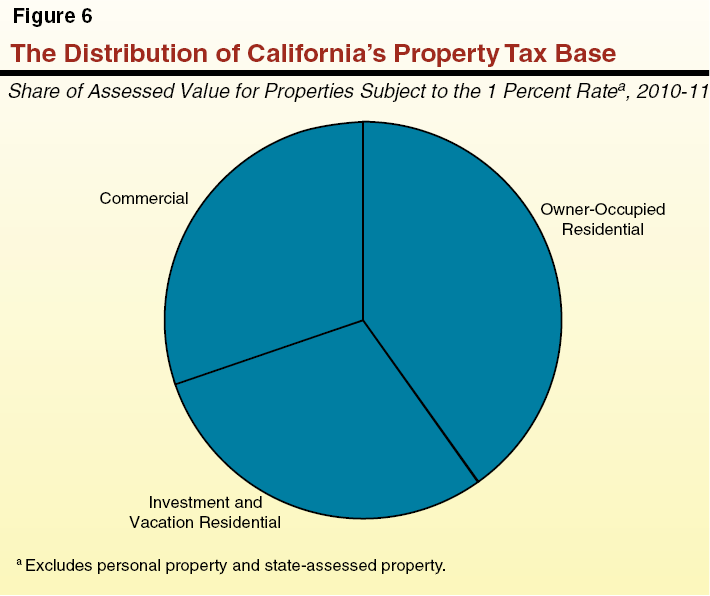

Owner–Occupied Residential. In 2010–11, there were 5.5 million owner–occupied homes in California with a total assessed value of $1.6 trillion. As shown in Figure 6, owner–occupied residential properties accounted for the largest share—39 percent—of the state’s tax base for the 1 percent rate.

Investment and Vacation Residential. Although the majority of residential properties are owner occupied, many others are investment or vacation properties such as multifamily apartments, rental condominiums, rental homes, vacant residential land, and vacation homes. (We classify vacant residential land and vacation homes as investment properties because they are an investment asset for the owner, even if he or she does not receive current income from them.) In 2010–11, there were 4.2 million investment and vacation residential properties. The assessed value of these properties was about $1.4 trillion, which represents 34 percent of the state’s total assessed value.

Commercial. In 2010–11, there were approximately 1.3 million commercial properties in California. This amount includes about 600,000 retail, industrial, and office properties (such as stores, gas stations, manufacturing facilities, and office buildings). It also includes 500,000 agricultural properties and 200,000 other properties (gas, oil, and mineral properties and the private use of public land). While commercial properties represent a relatively small share of the state’s total properties, they tend to have higher assessed values than other properties. Therefore, as shown in Figure 6, these properties (which have a total assessed value of $1.2 trillion) account for 28 percent of the state’s property tax base.

Has the Distribution of the Property Tax Base Changed Over Time?

There is little statewide information regarding the composition of California’s property tax base over time. Based on the available information, however, it appears that homeowners may be paying a larger percentage of total property taxes today than they did decades ago. We note, for example, that the assessed value of owner–occupied homes has increased from a low of 32 percent of statewide assessed valuation in 1986–87 to a high of 39 percent in 2005–06. (The share was 36 percent in 2011–12.) It also appears likely that owners of commercial property are paying a smaller percentage of property taxes than they did decades ago. For example, Los Angeles County reports that the share of total assessed value represented by commercial property in the county declined from 40 percent in 1985 to 30 percent in 2012. In addition, the assessed value of commercial property in Santa Clara County has declined (as a share of the county total) from 29 percent to 24 percent since 1999–00.

What Factors May Have Contributed to Changes in the Property Tax Base?

Various economic changes that have taken place over time probably have contributed to changes to California’s property tax base. For example, investment in residential property has increased significantly since the mid–1970s. Newly built single–family homes have become larger and are more likely to have valuable amenities than homes built earlier. As a result, new homes are more expensive to build and assessed at higher amounts than older homes. Over the same period, commercial activity in California has shifted away from traditional manufacturing, which tends to rely heavily on real property. Newer businesses, on the other hand, are more likely to be technology and information services based. These businesses tend to own less real property than traditional manufacturing firms do. (Technology and information services firms, however, rely heavily on business personal property—for example, computing systems, design studios, and office equipment—that are taxed as personal property and not included in the distribution of the state’s real property tax base.)

It also is possible that Proposition 13’s acquisition value assessment system has played a role in the changes to California’s tax base. Specifically, under Proposition 13, properties that change ownership more frequently tend to be assessed more closely to market value than properties that turn over less frequently. (Because properties are assessed to market value when they change ownership, properties that have not changed ownership in many years tend to have larger gaps between their assessed values and market values.) It is possible that some categories of properties change ownership more frequently than others and this could influence the composition of the overall tax base. The limited available research suggests that investment and vacation residential properties change ownership more frequently than commercial or owner–occupied residential property, indicating that they may be assessed closer to market value than other types of property.

How Much Revenue Is Collected?

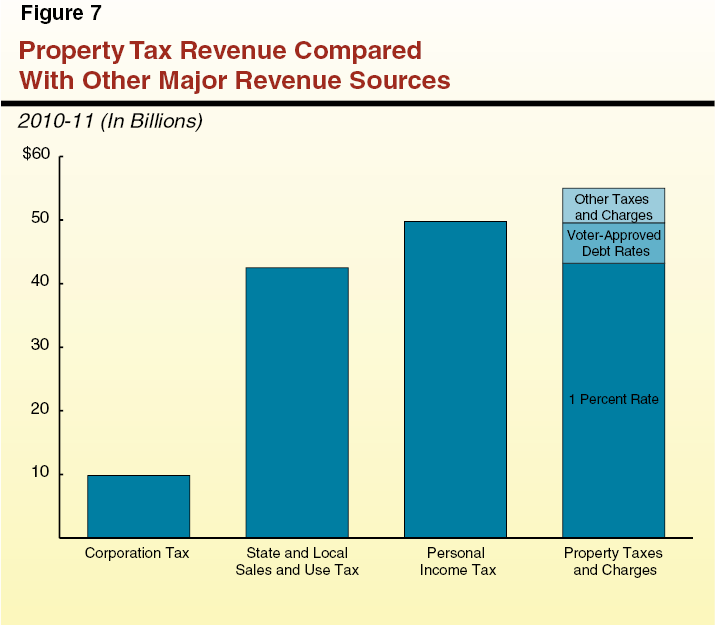

In 2010–11, California property tax bills totaled $55 billion. As shown in Figure 7, this amount included $43.2 billion under the 1 percent rate and $5.7 billion from voter–approved debt rates, making ad valorem property taxes one of California’s largest revenue sources.

Comparatively little is known about the remaining $6 billion of other taxes and charges on the property tax bill. From various reports summarizing local government finances, elections, and bond issuances, it appears that most of this $6 billion reflects property assessments, parcel taxes, and Mello–Roos taxes, though statewide data are not available on the exact amounts collected for each of these funding sources.

How Is the Revenue Distributed?

California property owners pay their property tax bills to their county tax collector (sometimes called the county treasurer–tax collector). The funds are then transferred to the county auditor for distribution. The county auditor distributes the funds collected from the 1 percent rate differently than the funds collected from the other taxes and charges on the bill. Specifically, the 1 percent rate is a shared revenue source for multiple local governments.

This section describes the distribution of revenue raised under the 1 percent rate and summarizes the limited available information regarding the distribution of voter–approved debt rates and non–ad valorem property taxes and charges.

Revenue From the 1 Percent Rate Is Shared by Many Local Governments

The 1 percent rate generates most of the revenue from the property tax bill—roughly $43 billion in 2010–11. On a typical property tax bill, however, the 1 percent rate is listed as the general tax levy or countywide rate with no indication as to which local governments receive the revenue or for what purpose the funds are used. In general, county auditors allocate revenue from the 1 percent rate to a variety of local governments within the county pursuant to a series of complex state statutes.

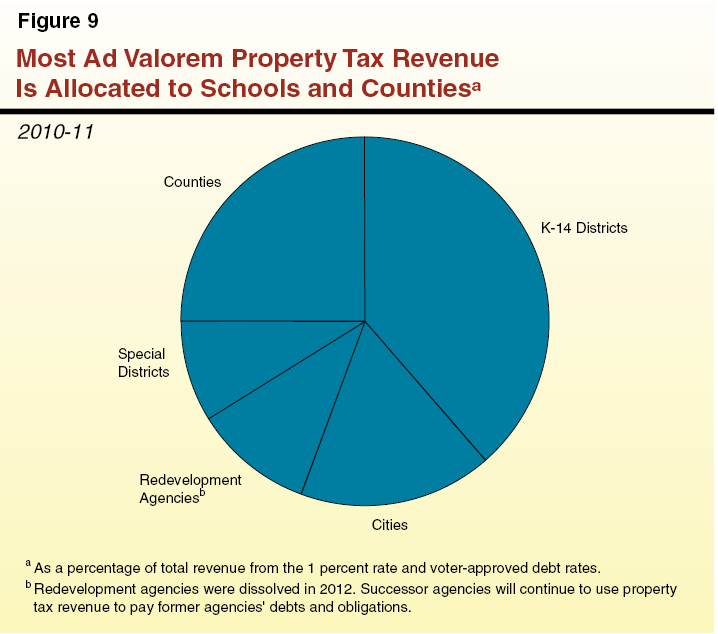

More Than 4,000 Local Governments Receive Revenue From the 1 Percent Rate. All property tax revenue remains within the county in which it is collected to be used exclusively by local governments. As shown in Figure 8, property tax revenue from the 1 percent rate is distributed to counties, cities, K–12 schools, community college districts, and special districts. Until recently, redevelopment agencies also received property tax revenue. As described in the nearby box, redevelopment agencies were dissolved in 2012, but a large amount of property tax revenue continues to be used to pay the former agencies’ debts and obligations.

Figure 8

How Many Local Governments Receive Revenue From the 1 Percent Rate?

Type of Local Government | Number |

Counties | 58 |

Cities | 480 |

Schools and Community Colleges | |

K–12 school districts | 966 |

County Offices of Education | 56 |

Community college districts | 72 |

Special Districts | |

Fire protection | 348 |

County service area | 316 |

Cemetery | 241 |

Community services | 201 |

Maintenance | 136 |

Highway lighting | 117 |

County water | 100 |

Recreation and park | 85 |

Hospital | 64 |

Sanitary | 60 |

Irrigation | 46 |

Mosquito abatement | 43 |

Public utility | 43 |

Othera | 400 |

Redevelopment Agenciesb | 422 |

Total | 4,254 |

a Thirty three other types of special districts report receiving property tax revenue from the 1 percent rate. These include county sanitation, municipal water, memorial, water authority, drainage, and library districts. b Dissolved in 2012. A portion of property tax revenue continues to pay these agencies’ debts and obligations. | |

Figure 9 shows the share of revenue received by each type of local government from the 1 percent rate and voter–approved debt rates. (As described later in the report, however, these shares vary significantly by locality.)

Redevelopment and Successor Agencies

More than 60 years ago, the Legislature established a process whereby a city or county could declare an area to be blighted and in need of redevelopment. After this declaration, most property tax revenue growth from the redevelopment “project area” was distributed to the redevelopment agency, instead of the other local governments serving the project area. As discussed in our report, The 2012–13 Budget: Unwinding Redevelopment, redevelopment agencies were dissolved in February 2012. Prior to their dissolution, however, redevelopment agencies received over $5 billion in property tax revenue annually. These monies were used to pay off tens of billions of dollars of outstanding bonds, contracts, and loans.

In most cases, the city or county that created the redevelopment agency is managing its dissolution as its successor agency. The successor agency manages redevelopment projects currently underway, pays existing debts and obligations, and disposes of redevelopment assets and properties. The successor agency is funded from the property tax revenue that previously would have been distributed to the redevelopment agency. As a result, even though redevelopment agencies have been dissolved, some property tax revenue continues to be used to pay redevelopment’s debts and obligations. Over time, most redevelopment obligations will be retired and the property tax revenue currently distributed to successor agencies will be distributed to K–14 districts, counties, cities, and special districts.

Property Taxes Also Affect the State Budget. Although the state does not receive any property tax revenue directly, the state has a substantial fiscal interest in the distribution of property tax revenue from the 1 percent rate because of the state’s education finance system. Each K–12 district receives “revenue limit” funding—the largest source of funding for districts—from the combination of local property tax revenue under the 1 percent rate and state resources. Thus, if a K–12 district’s local property tax revenue is not sufficient to meet its revenue limit, the state provides additional funds. Community colleges have a similar financing system, in which each district receives apportionment funding from local property tax revenue, student fees, and state resources. In 2010–11, the state contributed $22.5 billion to K–12 revenue limits and community college apportionments, while the remainder ($14.5 billion) came from local property tax revenue (and student fees).

State Laws Direct Allocation of Revenue From the 1 Percent Rate. The county auditor is responsible for allocating revenue generated from the 1 percent rate to local governments pursuant to state law. The allocation system is commonly referred to as “AB 8,” after the bill that first implemented the system—Chapter 282, Statutes of 1979 (AB 8, L. Greene). In general, AB 8 provides a share of the total property taxes collected within a community to each local government that provides services within that community. Each local government’s share is based on its proportionate countywide share of property taxes during the mid–1970s, a time when each local government determined its own property tax rate and property owners paid taxes based on the sum of these rates. (The average property tax rate totaled about 2.7 percent.) As a result, local governments that received a large share of property taxes in the 1970s typically receive a relatively large share of revenue from the 1 percent rate under AB 8. (More detail on the history of the state’s property tax allocation system—including AB 8—is provided in the appendix of this report.)

Revenue Allocated by Tax Rate Area (TRA). The county auditor allocates the revenue to local governments by TRA. A TRA is a small geographical area within the county that contains properties that are all served by a unique combination of local governments—the county, a city, and the same set of special districts and school districts. A single county may have thousands of TRAs. While there is considerable variation in the steps county auditors use to allocate revenue within each TRA, typically the county auditor annually determines how much revenue was collected in each TRA and first allocates to each local government in the TRA the same amount of revenue it received in the prior year. Each local government then receives a share of any growth (or loss) in revenue that occurred within the TRA that year. Each TRA has a set of growth factors that specify the proportion of revenue growth that goes to each local government. These factors—developed by county auditors pursuant to AB 8—are largely based on the share of revenue each local government received from the TRA during the late 1970s.

Figure 10 shows sample growth factors for TRAs in two California cities. As the figure indicates, 23 percent of any growth in revenue from the 1 percent rate in the sample TRA for Norwalk would be allocated to the county, 7 percent would go to the city, and the rest would be allocated to various educational entities and special districts. The percentage of property tax growth allocated to each type of local government can vary significantly by TRA. For example, Walnut Creek’s K–12 school district receives 33 percent of the growth in revenue within its TRA while Norwalk’s school district receives only 19 percent from its TRA. As noted above, this variation is based largely on historical factors specified in AB 8.

Figure 10

Allocation of Property Tax Growth in Sample Tax Rate Areas

Norwalk, Los Angeles Countya | Percent Share |

Los Angeles County | 23% |

Educational Revenue Augmentation Fund | 20 |

Norwalk–La Mirada Unified School District | 19 |

Los Angeles County Fire Protection District | 18 |

City of Norwalk | 7 |

Norwalk Parks and Recreation District | 3 |

Los Angeles County Library | 2 |

La Mirada Parks and Recreation District | 2 |

Cerritos Community College District | 2 |

Los Angeles County Flood Control District | 1 |

Los Angeles County Sanitation District | 1 |

Greater Los Angeles County Vector Control | —b |

Water Replenishment District of Southern California | —b |

Little Lake Cemetery District | —b |

Los Angeles County Department of Education | —b |

100% | |

Walnut Creek, Contra Costa Countyc | Percent Share |

Mount Diablo Unified School District | 33% |

Educational Revenue Augmentation Fund | 17 |

Contra Costa County | 13 |

Contra Costa County Fire | 13 |

City of Walnut Creek | 9 |

Contra Costa Community College District | 5 |

East Bay Regional Park District | 3 |

Contra Costa County Library | 2 |

Central Contra Costa Sanitary District | 2 |

Contra Costa County Office of Education | 1 |

Contra Costa County Flood Control | 1 |

Bay Area Rapid Transit | 1 |

Contra Costa Water District | 1 |

Contra Costa County Water Agency | —b |

Contra Costa County Resource Conservation District | —b |

Contra Costa County Mosquito Abatement District | —b |

Contra Costa County Service Area R–8 | —b |

Bay Area Air Management District | —b |

100% | |

a Percentages indicate allocation of the growth in property taxes in Los Angeles County tax rate area 06764. b Less than 0.5 percent. c Percentages indicate allocation of the growth in property taxes in Contra Costa County tax rate area 09025. | |

Some Revenue Is Allocated to a Countywide Account—ERAF. Most of the revenue from the 1 percent rate collected within a TRA is allocated to the city, county, K–14 districts, and special districts that serve the properties in that TRA. State law, however, directs the county auditor to shift a portion of this revenue to a countywide account that is distributed to other local governments that do not necessarily serve the taxed properties. The state originally established this account—the Educational Revenue Augmentation Fund (ERAF)—to provide additional funds to K–14 districts that do not receive sufficient property tax revenue to meet their minimum funding level. State laws later expanded the use of ERAF to include reimbursing cities and counties for the loss of other local revenue sources (the vehicle license fee and sales tax) due to changes in state policy. For example, Figure 10 shows that 20 percent of any revenue growth within Norwalk’s TRA is deposited into ERAF. It is possible that some or all of this revenue could be allocated to a city or K–14 district in a different part of Los Angeles County.

Most Revenue From Voter–Approved Debt Distributed to Schools

Voter–approved debt rates are levied on property owners so that local governments can pay the debt service on voter–approved general obligation bonds (and pre–1978 voter–approved obligations). The state’s K–12 school districts receive the majority of the revenue from voter–approved debt rates ($3.1 billion of $5.2 billion in 2009–10). The amount received by cities ($520 million), special districts ($470 million), and counties ($320 million) is significantly less. The amount of taxes collected to pay voter–approved debt varies considerably across the state. For example, the average amount paid by an Alameda County property owner for voter–approved debt rates is about $2 for each $1,000 of assessed value, while the average amount paid in some counties is less than 10 cents per $1,000 of assessed value.

Limited Information About Distribution Of Other Property Taxes and Charges

Less information is available about the statewide distribution of the revenue from parcel taxes, Mello–Roos taxes, and assessments.

Parcel Taxes. Recent election reports and financial data suggest that parcel taxes represent a significant and growing source of revenue for some local governments. Specifically, between 2001 and 2012, local voters approved about 180 parcel tax measures to fund cities, counties, and special districts, and about 135 measures to fund K–12 districts. The most recent K–12 financial data (2009–10) indicate that schools received about $350 million from this source. We were not able to locate information on the statewide amount of parcel tax revenue collected by cities, counties, and special districts.

Mello–Roos Taxes. Mello–Roos districts are required to report on their bond issuance, which provides some information about the types of local governments that receive Mello–Roos tax revenue. It is likely that local governments issuing a large amount of Mello–Roos bonds also are collecting a large amount of Mello–Roos tax revenue. Between 2004 and 2011, cities issued about 50 percent of the bonds issued by Mello–Roos districts in California, followed by K–12 districts at about 30 percent. During the same time period, the issuance of Mello–Roos bonds was concentrated in specific regions, as more than 60 percent of the bonds were issued by local governments in four counties—Riverside, Orange, San Diego, and Placer.

Assessments. Most of the property improvements funded by assessments are provided by cities and special districts. In 2009–10, cities and special districts reported receiving $760 million and $650 million, respectively, in revenue from assessments. In contrast, counties reported $11 million in such revenues.

Why Do Local Government Property Tax Receipts Vary?

The share of revenue received by each type of local government from the 1 percent rate varies significantly by locality. County governments, for example, receive as little as 11 percent (Orange) and as much as 64 percent (Alpine) of the ad valorem property tax revenue collected within their county. As shown in Figure 11, revenue raised from the 1 percent rate also varies considerably by locality when measured by revenue per resident. Orange County receives about $175 per resident, while four counties receive more than $1,000 per resident. Although cities, on average, receive about $240 per resident in revenue from the 1 percent rate, some receive more than $500 per resident and many receive less than $150 per resident. School districts also receive widely different amounts of property taxes per enrolled student, with an average of just under $2,000. (As noted above, the state “tops off” school property tax revenue with state funds to bring most schools to similar revenue levels.) Finally, special districts also receive varying amounts of property tax revenue, though data limitations preclude us from summarizing this variation on a statewide basis.

Figure 11

Property Tax Receipts From the 1 Percent Rate for Selected Local Governments

2009–10

Cities | Property Taxes per Resident | Counties | Property Taxes per Resident | Schoolsa | Property Taxes per Student |

Industry | $2,541 | San Franciscob | $1,411 | Mono | $10,683 |

Malibu | 559 | Sierra | 1,126 | San Mateo | 5,432 |

Mountain View | 344 | Inyo | 876 | Marin | 5,213 |

Los Angeles | 332 | Napa | 522 | San Francisco | 4,020 |

Long Beach | 268 | El Dorado | 464 | Orange | 3,315 |

Oakland | 250 | Los Angeles | 359 | San Diego | 2,760 |

State Average | 242 | State Average | 320 | State Average | 1,960 |

San Jose | 200 | Alameda | 301 | Yolo | 1,765 |

Fresno | 183 | Sacramento | 286 | Sacramento | 1,344 |

Anaheim | 167 | Contra Costa | 271 | San Joaquin | 1,163 |

Santa Clarita | 140 | San Diego | 261 | Los Angeles | 1,142 |

Chico | 129 | Riverside | 200 | Fresno | 810 |

Modesto | 119 | Orange | 174 | Kings | 379 |

a Countywide average for K–12 schools. b San Francisco is a city and a county. | |||||

Three factors account for most of this variation in local government property tax receipts. We discuss these factors below.

Variation in Property Values

California has a diverse array of communities with large variation in land and property values. Some communities are extensively developed and have many high–value homes and businesses, whereas others do not. Because property taxes are based on the assessed value of property, communities with greater levels of real estate development tend to receive more property tax revenue than communities with fewer developments. For example, high–density cities generally receive more property tax revenue than rural areas due to the greater level of development. Coastal and resort areas also typically receive more property taxes due to the high property values. Certain high–value properties—such as a power plant or oil refinery—also increase property tax revenue. Alternatively, localities with large amounts of land owned by the federal government, universities, or other organizations that are not required to pay property taxes may receive less revenue.

Prior Use of Redevelopment

Prior decisions by cities and counties to use redevelopment also influences the amount of property tax revenue local governments receive. Prior to the dissolution of redevelopment agencies in 2012, most of the growth in property taxes from redevelopment project areas went to the redevelopment agency, rather than other local governments. A large share of property tax revenue now goes to successor agencies to pay the former redevelopment agencies’ debts and obligations. The use of redevelopment varied extensively throughout the state. In those communities with many redevelopment project areas, the share of property tax revenue going to other local governments is less than it would be otherwise. In places with large redevelopment project areas—such as San Bernardino and Riverside counties—more than 20 percent of the county’s property tax revenue may go to pay the former redevelopment agencies’ debts and obligations.

State Allocation Laws Reflecting 1970s Taxation Levels

Finally, the amount of property taxes allocated to local governments depends on state property tax allocation laws, principally AB 8. As discussed earlier in this report (and in more detail in the appendix), the AB 8 system was designed, in part, to allocate property tax revenue in proportion to the share of property taxes received by a local government in the mid–1970s. Under this system, local governments that received a large share of property taxes in the 1970s typically continue to receive a relatively large share of property taxes today. Although there have been changes to the original property tax allocation system contained in AB 8, the allocation system continues to be substantially based on the variation in property tax receipts in effect in the 1970s.

This variation largely reflects service levels provided by local governments in the 1970s. Local governments providing many services generally collected more property taxes in the 1970s to pay for those services. As a result, those local governments received a larger share of property taxes under AB 8. For example, cities and counties that provided many government services, including fire protection, park and recreation programs, and water services, typically receive more property tax revenue than governments that relied on special districts to provide some or all of these services.

Are There Concerns About How Property Taxes Are Distributed?

While no system for sharing revenues among governmental entities is perfect, the state’s system for allocating property tax revenue from the 1 percent rate raises significant concerns about local control, responsiveness to modern needs, and transparency and accountability to taxpayers. We discuss these concerns separately below and then address the question: Could the state change the allocation system?

Lack of Local Control

Unlike local communities in other states, California residents and local officials have virtually no control over the distribution of property tax revenue to local governments. Instead, all major decisions regarding property tax allocation are controlled by the state. Accordingly, if residents desire an enhanced level of a particular service, there is no local forum or mechanism to allow property taxes to be reallocated among local governments to finance this improvement. For example, Orange County currently receives a very low share of property taxes collected within its borders—about 11 percent. If Orange County residents and businesses wished to expand county services, they have no way to redirect the property taxes currently allocated to other local governments. Their only option would be to request the Legislature to enact a new law—approved by two–thirds of the members of both houses—requiring the change in the property tax distribution. In other words, local officials have no power to raise or lower their property tax share on an annual basis to reflect the changing needs of their communities. As a result, if residents wish to increase overall county services, they would need to finance this improvement by raising funds through a different mechanism such as an assessment or special tax.

Limited Transparency and Accountability

The state’s current allocation system also makes it difficult for taxpayers to see which entities receive their tax dollars. Property tax bills note only that a bulk of the payment goes to the 1 percent general levy. Even if taxpayers do further research and locate the AB 8 local government sharing factors for their TRA, it is difficult to follow the actual allocation of revenue because the fund shifts related to ERAF and redevelopment complicate this system.

In addition to making it difficult for taxpayers to determine how their tax dollars are distributed, the AB 8 system reduces government accountability. The link between the level of government controlling the allocation of the tax (the state) and the government that spends the tax revenue (cities, counties, special districts, and K–14 districts) is severed. For example, if a taxpayer believes the level of services provided by an independent park district is inadequate, it is difficult to hold the district entirely accountable because the state is responsible for determining the share of property taxes allocated to the district.

Limited Responsiveness to Modern Needs and Preferences

An effective tax allocation system ensures that local tax revenue is allocated in a way that reflects modern needs and preferences. In many ways, California’s property tax allocation system—which remains largely based on allocation preferences from the 1970s—does not meet this criterion. California’s population and the governance structure of many local communities have changed significantly since the AB 8 system was enacted. For example, certain areas with relatively sparse populations in the 1970s have experienced substantial growth and many local government responsibilities have changed. One water district in San Mateo County—Los Trancos Water District—illustrates the extent to which the state’s property tax allocation system continues to reflect service levels from the 1970s. Specifically, this water district sold its entire water distribution system to a private company in 2005, but continues to receive property tax revenue for a service it no longer provides.

Changing the Allocation System Is Difficult

Over the years, the Legislature, local governments, the business community, and the public have recognized the limitations inherent in the state’s property tax allocation system. Despite the large degree of consensus on the problems, major proposals to reform the allocation system have not been enacted due to their complexity and the difficult trade–offs involved. Because California has thousands of local governments—many with overlapping jurisdictions—reorienting the property tax allocation system would be extraordinarily complex. Updating the AB 8 property tax sharing methodology would require the Legislature to determine the needs and preferences of each California community and local government. This would be a difficult—if not impossible—task to undertake in a centralized manner. Alternatively, the state could allow the distribution of the property tax to be carried out locally, but there is no consensus about what process local governments would use to allocate property taxes among themselves. Whether done centrally or locally, any reallocation is difficult because providing additional property tax receipts to one local government would require redirecting it from another local government or amending the Constitution. In addition, any significant change to the allocation of property tax revenue would require approval by two–thirds of the Legislature due to provisions in the Constitution added by Proposition 1A (2004). (These issues are discussed further in the appendix.)

What Are the Strengths and Limitations of California’s Property Tax System?

For many years, California’s overall property tax system—the types of taxes paid by property owners and the determination of property owner tax liabilities—has evoked controversy. Some people question whether the distribution of the tax burden between residential and commercial properties is appropriate and whether the amount of taxes someone pays should depend, in part, on how long he or she has owned the property. Other people praise the financial certainty that the tax system gives property owners. From one year to the next, property owners know that their tax liabilities under the 1 percent rate will increase only modestly. In this section, we do not attempt to resolve this long–standing debate. Instead, we review property taxes by looking at how they measure according to five common tax policy criteria—growth, stability, simplicity, neutrality, and equity. Using this framework, we highlight particular aspects of the state’s property tax system, both its strengths and limitations, for policymakers and other interested parties.

Economists use the five common tax policy criteria summarized in Figure 12 to objectively compare particular taxes. These criteria relate to how taxes affect people’s decisions, how they treat different taxpayers, and how the revenue raised from taxes performs over time. In practice, all taxes involve trade–offs. Sometimes the trade–offs are between two tax policy criteria. For example, revenue sources that grow quickly may be less stable from one year to the next than other revenue sources. Other times, the trade–offs are between tax policy criteria and other governmental policy objectives that may not be directly related to one of the five tax criteria. For example, one such trade–off might be that ensuring that a property owner’s taxes do not increase dramatically from one year to the next (a reasonable governmental policy objective) can result in a tax system in which the owners of similar properties are taxed much differently (contrary to the equity criteria of tax policy).

Figure 12

Common Economic Criteria for Evaluating Tax Systems

|

|

|

|

|

What Factors Affect Property Tax Growth Each Year?

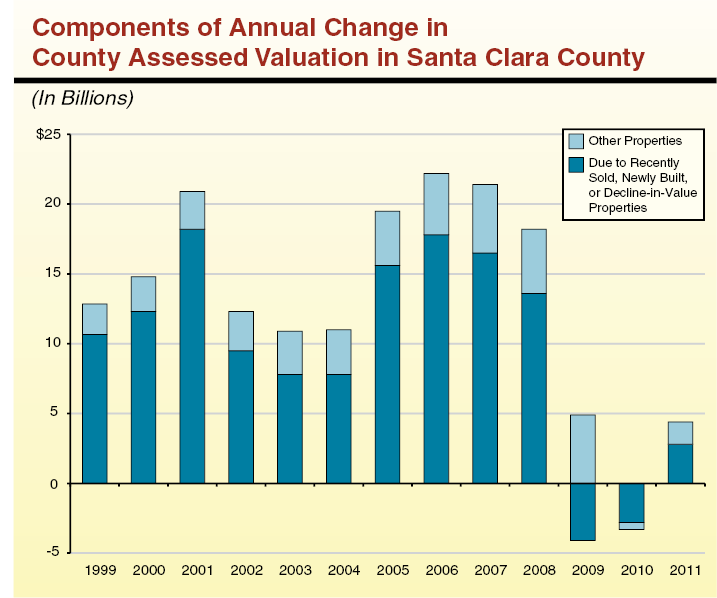

Most of the annual change in property tax revenues is the result of large changes in assessed value that affect a small number of properties, including:

- Recently Sold Properties. When a property sells, its assessed value resets to the purchase price. This represents additional value that is added to the tax base because the sale price of the property is often much higher than its previous assessed value.

- Newly Built Property and Property Improvements. New value is added to the county’s tax base when new construction takes place or improvements are made—mainly additions, remodels, and facility expansions—because structures are assessed at market value the year that they are built.

- Proposition 8 (1978) Decline–in–Value Properties. These properties contribute significantly to growth or decline in a county’s tax base because their assessed values may increase or decrease dramatically in any year. A particularly large impact on assessed valuation tends to occur in years when a large number of these properties transfer from Proposition 13 assessment to reduced assessment.

As shown by the dark bars in the figure below, recently sold, newly built, and decline–in–value properties typically account for more than two–thirds of total changes in countywide assessed value in Santa Clara County. Other properties, although they represent most of the properties in the county’s tax base, contribute less because the growth of these properties’ assessed values is limited to 2 percent per year.

What Factors Affect Property Tax Stability?

Acquisition Value Assessment System Contributes to Revenue Stability.The main reason California’s property tax revenue is stable is that the assessed value of most properties increases each year by a maximum of 2 percent. In any given year, only a small fraction of properties are sold and reset to market value. This means that real estate conditions affect a relatively small portion of the tax base each year, insulating property tax revenue from year–to–year real estate fluctuations.

Proposition 8 (1978) Decline–in–Value Properties Reduce Revenue Stability. As noted earlier in the report, county assessors may reduce a property’s assessed value in the event that its market value falls below its assessed value. Each year thereafter, the property is assessed at market value until it rises above what its assessed value would have been had it remained at its acquisition value adjusted upward each year at a maximum of 2 percent. During 2010–11, more than one in four properties in California was temporarily assessed to market value. Because these properties are assessed each year at market value, they link the property tax base more closely to the local real estate market than other properties, thereby reducing the property tax’s stability somewhat.

Revenue Growth

From government’s perspective, revenue sources that grow along with the economy are preferable because they can provide resources sufficient to maintain current services. This can help governments avoid increasing existing taxes or taxing additional activities in order to meet current service demands.

The Property Tax Has Grown Faster Than the Economy. Personal income in California—an approximate measure of the size of the state’s economy—has grown at an average annual rate of 6.3 percent since 1979. Over the same period, revenue from the 1 percent property tax rate has grown at an average annual rate of 7.3 percent. As we describe in the nearby box, much of the growth in property tax revenue depends on new construction and property sales.

The Growth of Parcel and Mello–Roos Tax Revenues Depends on the Structure of the Tax. The terms of parcel taxes and Mello–Roos taxes vary by locality. Some local governments have taxes with escalation clauses or other provisions that modify the amount of the tax as local government costs change. Other parcel taxes and Mello–Roos taxes are set at fixed amounts per parcel. Depending on their structure, these taxes may or may not provide local governments with a growing source of revenue.

Revenue Stability

Revenue sources that remain relatively stable from one year to the next help governments manage economic downturns, which tend to reduce revenue and at the same time increase demand for certain public services. Stable revenue sources also may help governments plan more effectively for future needs, including long–term investments in transportation, education, and public safety.

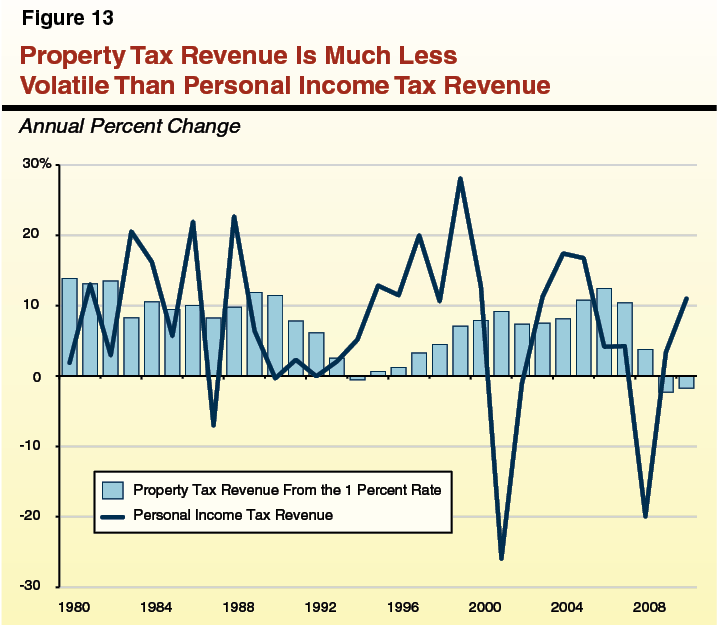

The Property Tax Is a Stable Revenue Source. Despite being linked to the volatile real estate market, the property tax is California’s most stable major revenue source. Since 1979, as shown in Figure 13, personal income tax revenue has been three times more volatile, on average, than property tax revenue from the 1 percent rate. During the same period, statewide property tax revenue has declined in only three years, 1994–95, 2009–10, and 2010–11.

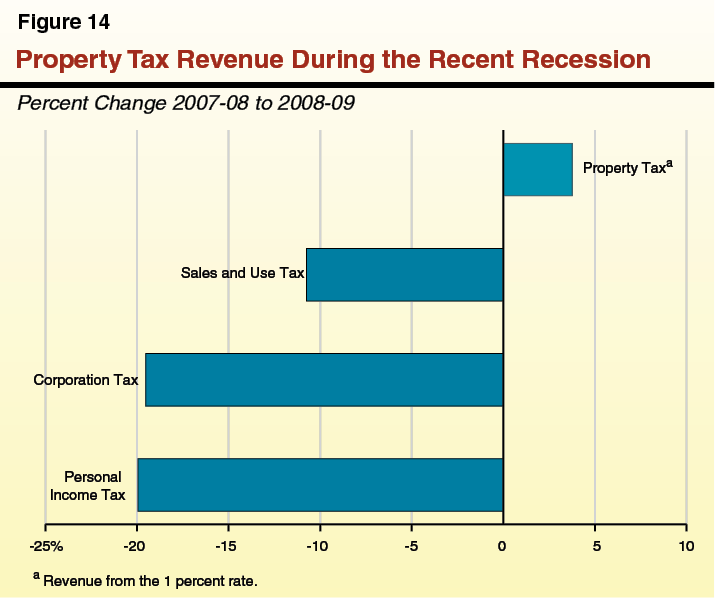

The Property Tax Was More Stable Than Other Revenue Sources During the Recent Recession. As shown in Figure 14, revenue from the 1 percent property tax rate fared comparatively well during the most recent recession. (In the nearby box, we discuss why the property tax is stable.) Changes in property tax revenue tend to lag economic trends by one or more years because of the state’s acquisition value assessment system and the lengthy period between when most properties are assessed (January) and when property tax payments are due (December of that year and April of the next).

Parcel Taxes and Mello–Roos Taxes Also Are Stable. Because most parcel and Mello–Roos taxes are set at fixed amounts per parcel, there is minimal year–to–year fluctuation in the revenues that they raise.

Assessed Valuation in Some Counties, However, Has Declined Significantly. Though statewide property tax revenue has remained comparatively stable throughout the recent recession, some areas of the state have experienced considerable declines in their property tax base. These counties tend to have a large proportion of their properties under Proposition 8 decline–in–value assessments and have high foreclosure rates. For example, Riverside County had the second highest number of foreclosures (17,000) among counties and more than 400,000 decline–in–value properties in 2011. Partly as a result of these trends, total assessed value in Riverside County declined by 15 percent between 2008 and 2011.

Simplicity

A well–designed tax system should be simple for taxpayers to understand and easy and inexpensive for governments to administer. Complex tax systems can be expensive for governments to administer effectively and may be confusing, time–consuming, and costly for taxpayers.

Most of the costs associated with administering the state’s property tax system (ad valorem property taxes, parcel taxes, and Mello–Roos taxes) reflect the activities by county assessors, tax collectors, and auditors. While comprehensive data on these costs are not available, total property tax administration costs likely are between 1.5 percent and 2 percent of collections, a somewhat higher level than that of state tax agencies that perform similar functions. A significant component of the property tax’s administrative cost is from counties’ responsibility to allocate property taxes to local governments pursuant to increasingly complex state laws. County costs related solely to determining property values, the other main component of administration, were slightly less than 1 percent of total revenues collected in 2010–11—a percentage similar to that of state tax agencies.

From the taxpayers’ perspective, the property tax is generally a simple tax with which to comply. Tax payments are due in equal installments twice per year. And, in most years, the assessed value of real property grows automatically by a maximum of 2 percent. Reassessments based on market value (which taxpayers are more likely to appeal) occur infrequently for most property owners.

The property tax assessed on personal property is typically more administratively cumbersome for owners and assessors. This is because personal property is assessed annually at market value using complex depreciation schedules. These assessments, therefore, are more likely to be appealed, a process that can take more than a year to resolve.

Neutrality

Nearly all taxes alter taxpayer behavior to some degree. Economists agree, however, that in most cases the ideal tax system is one that alters decisions—about what goods to buy, what products to make, and where to work or live—as little as possible. Economists prefer these “economically neutral” taxes because they assume that people and businesses are in the best position to make consumption, savings, and investment decisions that meet their economic and personal needs. Tax policies that influence what people buy and what businesses produce tend to distance people and businesses from their preferred choices, leaving them less well off than they would be if the tax system were economically neutral. Policymakers design some taxes, on the other hand, to influence taxpayer behavior in a way that promotes or discourages particular activities. In general, these should be well targeted and have strong justifications so that they achieve their policy goals with as little interference as possible in other personal decision making. Below, we describe how ad valorem property taxes may influence taxpayer behavior and then discuss the possible effects of parcel and Mello–Roos taxes.

Some Homeowners and Businesses May Move Less Frequently. California’s ad valorem property taxes may affect an individual’s decision to move because longer ownership results in a lower effective property tax rate. (An effective property tax rate differs from the 1 percent basic rate in that it is the amount of property taxes paid divided by the current market value of the property.) As shown in Figure 15, effective tax rates can vary considerably. New Owner A, for example, has an effective tax rate of 1 percent because the assessed value of his or her property is the same as its market value. Owners B and C, who have owned their properties longer than Owner A, have assessed values below their market values because their market values increased by more than 2 percent each year (and therefore faster than assessed values). As a result, most owners who have owned a property for many years pay an effective tax rate well below 1 percent. For those choosing to move, however, their effective tax rate is reset to 1 percent, producing a moving penalty that may influence some property owners’ relocation decisions. For example, established firms that benefit from their comparatively low effective property tax rates could be dissuaded from relocating—decisions that, absent the moving penalty, could benefit the companies financially. (As we discuss below, differing effective tax rates also affect the equity of the property tax.)

Figure 15

Hypothetical Effective Property Tax Rates for Three Property Owners

Year Purchased | Market Value | Assessed Value | Property Tax Rate | Property Tax Paid | Effective Tax Rate | |

Owner A | 2012 | $300,000 | $300,000 | 1% | $3,000 | 1.0% |

Owner B | 2002 | 300,000 | 180,000 | 1 | 1,800 | 0.6 |

Owner C | 1986 | 300,000 | 110,000 | 1 | 1,100 | 0.4 |

Homeowners and Businesses May Invest Less in Property Improvements. When a property undergoes improvements, the newly constructed portion of the property is assessed at its full market value. The existing property, on the other hand, is typically assessed below its current market value, meaning that improvements are taxed at a higher effective rate than existing property. Because improvements are subject to higher effective tax rates, the return on investment that businesses receive from new improvements is lower and the taxes that homeowners pay on them are higher than they would be if all property—new and existing—were taxed uniformly. This may lead some businesses and homeowners to invest less than they otherwise would in new property improvements.

Homeowners May Change Behavior in Response to Assessment Exclusions. Voters have approved ballot propositions that exclude some types of property transfers from triggering reassessment to market value. (These exclusions are summarized earlier in this report in Figure 2.) For example, residential property transfers between certain family members do not trigger reassessment. These exclusions could alter decisions homeowners make about their property. For example, a homeowner might transfer property to his or her child (thereby passing on his or her low effective property tax rate) when, absent the exclusion, the owner might have sold the property to a nonrelative. In turn, that child could find it more economical to rent the property (and benefit from the low effective property tax rate) than to sell (and forego the benefit of his or her low effective rate).

Equity

Equity relates to how taxes affect taxpayers with different levels of income or wealth. Economists use two different standards of equity—vertical and horizontal—to evaluate taxes. Vertical equity occurs when wealthier taxpayers pay a greater amount in taxes than less wealthy taxpayers. Horizontal equity, on the other hand, occurs when similar taxpayers—those with similar incomes or wealth—pay the same amount in taxes. Under an equitable property tax system (1) owners of highly valuable property pay more in taxes than owners of less valuable property and (2) the owners of two similar properties pay a similar amount in property taxes. Put differently, an equitable system would tax property owners at the same effective rate. As we discussed in the previous section, however, property owners often are subject to different effective tax rates. Therefore, California’s ad valorem property taxes, parcel taxes, and Mello–Roos taxes often do not meet these standards of equity.

Equity Reduced by Acquisition Value Assessment and 2 Percent Assessed Value Cap. California’s property tax system does not consistently meet the standards of horizontal or vertical equity. As discussed earlier in this report, two owners with identical properties may pay different amounts of property taxes if one owner bought the property a decade before the other. In a tax system with horizontal equity, both owners would pay similar amounts. In relation to vertical equity, the tax system’s reliance on acquisition value and the 2 percent cap on assessed valuation growth can result in owners of valuable property paying less than owners of (recently acquired) less valuable property. In a tax system with vertical equity, owners of valuable property would pay more in taxes because owners of valuable property generally are wealthier than owners of less valuable property.

Homeowners Who Are Mobile Pay Higher Effective Tax Rates. Homeowners who move often—military families, younger homeowners, or those with jobs that require them to relocate frequently—tend to have higher effective ad valorem tax rates than homeowners who move less frequently because newly purchased properties are assessed at market value. Relocation decisions may result from circumstances that households may not have foreseen, such as employment changes, divorce, or other changes in family composition. Under horizontal equity, in contrast, taxpayers pay similar taxes unless their household income, wealth, or consumption patterns differ.

Fixed–Rate Taxes Do Not Meet Vertical Equity Standard. Parcel taxes and Mello–Roos taxes typically meet the criteria of horizontal equity but not vertical equity because property owners typically are charged the same amounts—regardless of their wealth or their properties’ value.

Summary

Our comparison of California’s property tax system with common tax policy criteria found mixed results. The ad valorem taxes generally meet the goals of administrative simplicity and providing governments with a growing source of stable revenue, but often do not meet the goals of neutrality and equity. Specifically, California’s ad valorem tax system (1) may influence decisions property owners make about relocations and expansions and (2) treat similar taxpayers differently and wealthier taxpayers the same as less wealthy taxpayers.